So you have decided to buy a second home, one that will act as an investment rather than a holiday home. How do you go about starting the process and what do you have to consider when doing it?

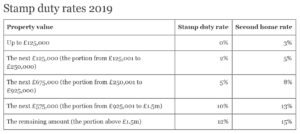

Firstly, you have to realise that the latest stamp duty rules mean that you will be expected to pay an extra 3% on top of the normal stamp duty rates. This is something that you will find almost impossible to avoid, despite some suggestions that you can. We have touched on these in the past but they are becoming increasingly tricky to enact. See below a helpful chart outlining the Stamp duty rates:

Once you have ascertained the rate of stamp duty to be paid you need to source the funding. If you are not using cash, and by that I mean the money you have in the bank account or stuffed under a mattress then you will need a buy to let mortgage. Banks and building societies now have tougher rules about who they’ll offer buy to let mortgages to. They’ll want to look at the rental income from the property you’re buying, as well as your income and personal circumstances so they can be certain you’ll keep up with repayments. These new rules have led to many people dropping out of the market, but they are there for good reason. Imagine a rate increase, or costs that you have not budgeted for hitting your income, including void months, something that in the rental market is difficult to avoid. All of these have made lenders nervous and as a result they have put in place tougher criteria. All that said there are now plenty of options on the table and plenty of mortgage providers in this sector, so as long as you meet the criteria, there is plenty to choose from.

A typical buy to let mortgage is an interest only type where during the life of the mortgage you are simply covering the interest charges leaving the capital to be paid off once the property is

sold. Repayment mortgage is not the norm in this sector, but can be used and is offered. On this type you are paying off both the interest and the capital, meaning that at the end of the term of the mortgage you will own the property. Obviously, this type of mortgage is more expensive and therefore not as popular, but is becoming more used as the tax laws around interest relief have changed over the last few years.

Once you have your funding and are ready to start looking, you need to choose an area that offers a good blend of income and growth. However, if this is the start of your journey you should be looking to build and one normally finds that initial investors tend to earn less income on their buy to let property from the outset as they use the rental to pay off the debt helping them to build a portfolio. Once you have decided where and the type of returns you want, you need to engage an independent property broker, one you can trust, and preferably one that has been recommended to you. Your broker should be able to point you in the right direction and will be able to offer you independent advice and present properties to you that are tailored to your specific requirements.

For more information and free advice about purchasing a second home for investment, speak to one of our senior brokers today.